Going ahead, the market is expected to remain positive despite intermittent consolidation, with investors focusing on the FOMC minutes, June quarter earnings, oil prices, and the progress of the monsoon.

Dalal Street Week Ahead

- Market expected to remain positive despite intermittent consolidation

- Investors to focus on FOMC minutes, June quarter earnings, oil prices, progress of the monsoon

- Tata Consultancy Services to kick start earnings season on July 9

The market gained nearly 0.9 percent during the week ended July 3, supported by easing concerns over the durability of the US-Iran peace arrangement and the situation around the Strait of Hormuz, as well as reduced expectations of a Fed funds rate hike following softer US labour market data.

Apart from the monsoon gaining strength across India, domestic sentiment received an additional boost from optimism surrounding the India-Japan summit, with investors anticipating progress in trade, defence, semiconductors, AI collaboration, and a proposed rupee-yen settlement framework.

Going ahead, the market is expected to remain positive despite intermittent consolidation, with investors focusing on the FOMC minutes, June quarter earnings, oil prices, and the progress of the monsoon.

The Nifty 50 rose 215 points (0.89 percent) to 24,271, while the BSE Sensex jumped 663 points (0.86 percent) to 77,764, extending their uptrend for a fourth consecutive week. Meanwhile, the Nifty Midcap 100 and Smallcap 100 indices gained 0.64 percent and 2.05 percent, respectively.

"Indian equities are expected to maintain a gradual uptrend, supported by favourable global cues and easing concerns over the US interest rate outlook," said Siddhartha Khemka, Head of Research, Wealth Management, at Motilal Oswal Financial Services.

According to Vinod Nair, Head of Research at Geojit Investments, market direction will be shaped by the US FOMC minutes, the start of the domestic earnings season, credit growth trends, and ongoing trade negotiations with Japan, the UK, and the US.

While risks persist amid downward revisions to earnings growth estimates, monsoon-related inflation concerns, and continued FII caution, much of the visible uncertainty appears to have already been priced in, leaving room for a constructive interpretation of incremental positive developments, he said.

Khemka added that investors will also closely monitor the southwest monsoon after June rainfall remained 40 percent below the Long Period Average (LPA). While the IMD has forecast July rainfall at 94 percent of the Long Period Average, it has revised its 2026 monsoon forecast to 90 percent of the Long Period Average due to El Niño conditions.

Here are 10 key factors to watch next week:

The much-awaited June quarter earnings (Q1FY27) season, which is expected to get impacted to some extent due to West Asia tensions, will start next week with Tata Consultancy Services being the first to announce its earnings on July 9.

Apart from TCS, LTM, L&T Finance, Avenue Supermarts, Anand Rathi Wealth, and GM Breweries will also release their quarterly numbers in the coming week.

The management commentaries with respect to full year outlook will be a key factor to watch in the entire earnings season, especially after the easing of Middle East tensions and falling oil prices.

2) FOMC Minutes

Globally, the key focus will be on the FOMC minutes on July 8, although the week ahead is relatively light on the economic releases front barring weekly jobless claims and S&P Global Services PMI, the only other notable releases. Markets assess the degree of internal division among Fed officials over the policy path highlighted in the June dot plot, while the recent soft jobs data reduced the possibility of Fed funds rate hike.

3) Global Economic Data

Apart from FOMC minutes, the market participants will also focus on monthly retail sales & PPI numbers from Europe, and China's inflation, PPI and vehicle sales data for the coming week.

4) Crude Oil Prices

Oil prices, which saw some stability with WTI and Brent closing the week modestly lower near $69 a barrel and $72 a barrel after four months of violent swings due to a steady recovery in tanker traffic through the Strait of Hormuz, will also be keenly watched as the change in prices impacts the oil importing nations like India the most globally. The sharp fall of around 37 percent since the high of May month provided major relief to the country, with Brent crude oil futures closing the week 0.26 percent down at $71.80 a barrel, the lowest closing level since February 16-20 which is a pre-war level.

Flows through the Strait of Hormuz climbed above 10 million barrels per day with American naval support, while UAE exports returned to pre-conflict levels.

The Doha talks concluded on Wednesday, with Qatar describing the discussions as making positive progress, although both sides remain at odds over Hormuz sovereignty and the unfreezing of Iranian funds. Iran has signalled that it will begin charging transit service fees for ships using the Strait from mid-August, which could lift shipping costs that the market has not yet fully priced in, Kaynat Chainwala of Kotak Securities said.

The next round of talks between US and Iran has been paused as Iran observes a mourning period for its late Supreme Leader through July 9.

5) Domestic Economic Data

Back home, the bank loan and deposit growth for week ended June 26, along with foreign exchange reserves for fortnight ended July 3 will be released on June 10.

6) FII Flow

The mood at the foreign investors' (FIIs) desk will also be watched going ahead, as most experts believe FIIs are expected to turn buyers in India soon given the falling oil prices by 37 percent since the high of May month, & weakening of the chip trade globally along with likely healthy earnings growth in second half of FY27 onward provided no major global concerns.

FIIs, so far, have been net sellers to the tune of over Rs 4,000 crore in the last week, and more than Rs 49,000 crore in June despite intermittent buying especially after easing West Asia tensions and profit booking in AI trades. However, Domestic Institutional Investors (DIIs) fully compensated FIIs' outflow as they net bought Rs 12,600 crore worth shares during the week and more than Rs 85,000 crore of buying in June.

"Going forward, FPI outflows are likely to decline. Crash in crude price to below $72 a barrel and the big inflows expected from the FCNR (B) deposits will bring India’s BoP deficit significantly down. This will help the rupee to stabilise and even appreciate, which in turn, will prevent big FPI selling," " V K Vijayakumar, Chief Investment Strategist at Geojit Investments said.

The weakening of the chip trade globally, and the significant correction in Kospi in particular, may even persuade FPIs to turn buyers in India, he added.

Meanwhile, the Indian rupee weakened by 0.95 percent during the week to 95.20 against the US dollar after a strength in the past two weeks. On other side, the US dollar index witnessed profit booking, falling 0.48 percent to 100.87 as soft jobs data reduced the Fed funds rate hike expectations, after rally in the previous two weeks.

7) IPO Action

After a busy schedule last week, the primary market action will be moderated for the coming week as only four IPOs are scheduled for opening compared to 10 public issues launch in previous week.

In the mainboard segment, cotton yarn maker Kusumgar will open its Rs 650-crore initial public offering (IPO) on July 8, followed by power transmission & distribution products manufacturer Laser Power & Infra's Rs 742-crore offer scheduled for opening on July 9.

SME segment will also see two IPOs with both Happy Steels, and Devson Catalyst opening for public subscription on July 9, while the subscription for IC Electricals Company public issue will remain open till July 7.

On the listing front, total 10 new companies will be availbale for trading on the bourses next week with two – Aastha Spintex, and Knack Packaging – in the mainboard segment. And other eight – Adon Agro Commodities, Teja Engineering Industries, Atharva Polyplast, Seemax Resources, Sampark India Logistics, Vinit Mobile, Kratikal Tech, and IC Electricals Company – will be on the SME platforms.

8) Technical View

Technically, the Nifty 50 has gradually been gaining strength despite consolidation as the index traded well above key moving averages (except 50-day EMA) with improving momentum indicators, while sustaining above the resistance trendline breakout. The 24,400 can be immediate resistance for the index as reclaiming and sustaining above it can open door for 24,600 (April high) followed 24,800 (61.8 percent Fibonacci retracement of correction from February high to April low), however, the 24,200-24,000 is expected to immediate key support zone, according to experts.

9) F&O Cues, India VIX

The weekly options data suggested that the 24,400-24,500 is expected to be hurdle zone for the Nifty 50, with 24,000-23,900 as a crucial support zone.

The 24,500 strike holds the maximum Call open interest, followed by the 24,400 and 24,300 strikes, with the maximum Call writing at the 24,300, 24,350 and 24,400 strikes, however, on the Put side, the maximum Put open interest was seen at the 24,000 strike, followed by the 23,900 and 24,200 strikes, with the maximum Put writing at the 24,300, 24,200 and 24,250 strikes.

Meanwhile, the Volatility Index, India VIX, fell 9.6 percent for the week to 11.79, the lowest closing level since the week of January 12-16 and witnessed weakness in the last five out of six weeks, signalling rising comfort for bulls.

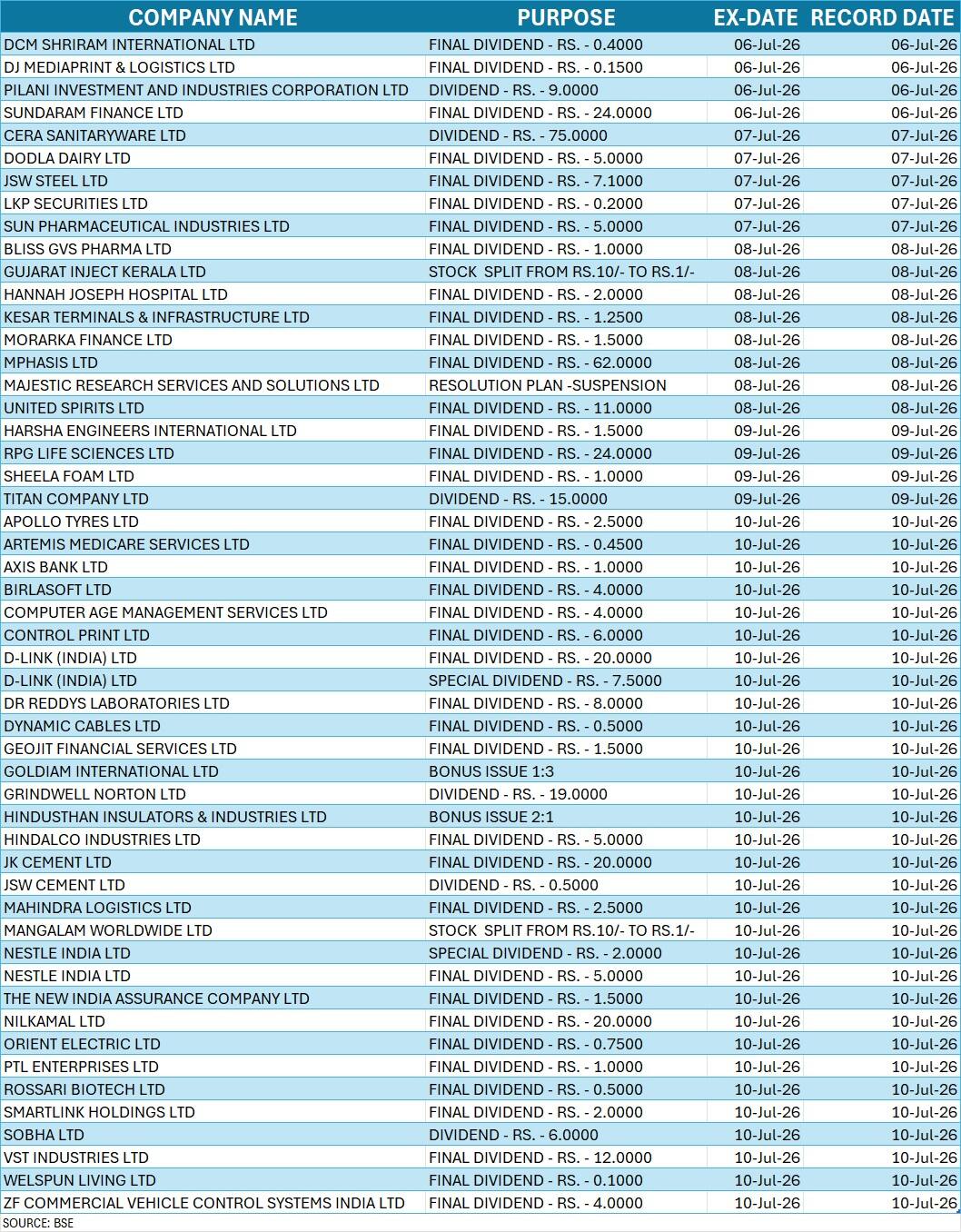

10) Corporate Action

Here are key corporate actions taking place next week:

Disclaimer: The views and investment tips expressed by experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.